As Singapore moves towards enhancing transparency and efficiency, companies are required to adopt the eXtensible Business Reporting Language (XBRL) in their financial reporting. This initiative has revolutionised the way companies communicate their financial information, streamlining the reporting process and providing stakeholders with a more accessible and standardised means of understanding financial data. This article will explore the XBRL requirement for financial reporting, pitfalls, formats and steps to perform your own XBRL filing.

Overview

- Understanding XBRL

- XBRL Requirement in Singapore

- Exemption from XBRL

- Types of XBRL Filing Formats

- Key Features of the XBRL Requirement

- How to File XBRL

- Common Mistakes in XBRL Filing

- Deadline for XBRL Filing

- How can we help?

Understanding XBRL:

XBRL is a global standard for financial reporting that allows information to be translated into a machine-readable format. It allows for an easy exchange and analysis of financial data, reducing the time and effort involved in preparing, analysing, and disseminating financial statements.

XBRL Requirement in Singapore:

The XBRL requirement in Singapore is applicable to all incorporated entities as mandated by the Accounting and Corporate Regulatory Authority (ACRA). This requirement aims to enhance the transparency and accessibility of financial information, ultimately contributing to a more informed and efficient financial ecosystem.

Depending on the company’s nature of business, revenue and asset criteria, the type of XBRL to be prepared and lodged with ACRA would vary.

Exemptions from XBRL:

With the majority of companies required to file the financial statements in XBRL, certain entities may be exempted. Exemptions are typically granted to companies that meet specific criteria, such as solvent Exempt Private Companies (EPC). However, exempted companies must still submit their financial statements in PDF format for regulatory scrutiny. Despite being exempt, companies may choose to lodge their financial statements in XBRL format voluntarily.

Types of XBRL Filing Formats:

Companies can filed their financial reporting in two formats – Full XBRL or Simplified XBRL - depending on the company’s revenue and asset size. Full XBRL requires the tagging of all financial data, providing a comprehensive view of the company's financial position. On the other hand, Simplified XBRL is a condensed version, highlighting key financial data that is applicable for smaller companies with simpler financial structures. Regardless of the type of XBRL, companies are expected to adhere to the XBRL requirement is essential to maintain regulatory compliance and promote transparency in financial reporting.

The main differences between a Full XBRL Format and Simplified XBRL Format is as follows:

|

Full XBRL Format |

Simplified XBRL Format |

| Comprehensive tagging of every financial data point. | Focused key financial elements. |

| Covers all aspects of financial statements and notes. |

Provides essential financial information, less detailed. |

| Applicable to all companies except exempt companies or those that qualify as Smaller Companies. |

Applicable to Smaller Companies meeting the following criteria:

|

Key Features of the XBRL Requirement:

Standardisation of Financial Reporting:

- Standardised format for financial statements, allows for consistency and comparability across different companies and industries.

- Streamlines the analysis process for regulators, investors, and other stakeholders.

Automated Data Analysis:

- One of the primary advantages of XBRL is its machine-readable nature that allows for automated data analysis.

- Regulatory bodies can quickly process and analyse large volumes of financial information, enhancing their oversight capabilities.

Enhanced Regulatory Compliance:

- The mandatory XBRL requirement in Singapore ensures that companies comply with a standardised reporting framework.

- This not only helps regulatory bodies in monitoring and enforcing compliance but also provides companies with a clear set of guidelines for financial reporting.

Improved Accessibility for Stakeholders:

- With the XBRL-formatted financial statements lodged to ACRA on an annual basis, it is more accessible to a wide range of stakeholders, including investors, analysts, and the general public.

- This increased accessibility promotes greater transparency and builds trust in the financial reporting process.

Cost and Time Efficiency:

- XBRL reduces the manual effort involved in preparing and reviewing financial statements, allowing companies to allocate resources more strategically.

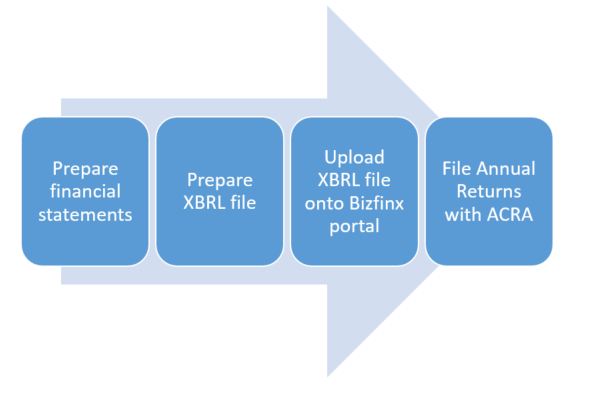

How to File XBRL:

Preparing the financial statements in XBRL format involves using specific software that allows for the tagging of financial data according to the taxonomy provided by ACRA. Companies can either engage a professional service provider or use ACRA's BizFinx self-help tool, to prepare and submit their XBRL reports.

Common Mistakes in XBRL Filing:

- Misidentifying or inaccurately tagging data points.

- Using an outdated or incorrect version of the taxonomy.

- Failing to tag comprehensive notes to financial statements.

- Missing filing deadlines or submitting incomplete reports.

- Using non-compliant XBRL software.

- Skipping on conducting thorough data validation before submission.

- Insufficient training for staff responsible for XBRL filing.

- Misunderstanding the application of accounting standards.

- Lack of a robust quality control process.

- Failing to map all relevant data points in financial statements.

Deadline for XBRL Filing:

Companies are required to file the XBRL at the point of filing their Annual Returns with ACRA.

Typically, a company is required to hold its Annual General meeting (AGM) within 6 months of its financial year end, and to file its Annual Returns with ACRA within 7 months of its financial year end.

Adhering to these deadlines is crucial to avoid penalties and maintain regulatory compliance.

How can we help?

As Singapore continues to position itself as a hub for business and finance, the XBRL requirement plays a crucial role in shaping a more resilient and accountable financial ecosystem. Companies can fulfil their regulatory obligations and also contribute to the potential for improved data analysis, reduced errors, and enhanced stakeholder communication.

Outsourcing the filing to a professional accounting services firm allows business owners to allocate valuable resources to focus on their business.

At AccountServe, our team of qualified and experienced professionals can assist your business with filing of financial statements and XBRL requirements.